.png)

When Growth Isn't Growth -The Gold Loan Illusion

- MS Blogs

- 3 days ago

- 3 min read

Updated: 1 day ago

India’s gold loan sector recently has, by most conventional measures, delivered strong outcomes.

Since FY 23 companies such as Muthoot Finance have reported:

Revenue Growth of around 36% CAGR

Profit growing at 39% CAGR

And an operating profit growth at 39% CAGR

What stands out is that this growth has come from a product backed by one of the most liquid forms of collateral yet consistently priced at relatively high yields.

At a glance, the picture holds together. The more useful question is what is actually driving it.

The Question Beneath the Numbers

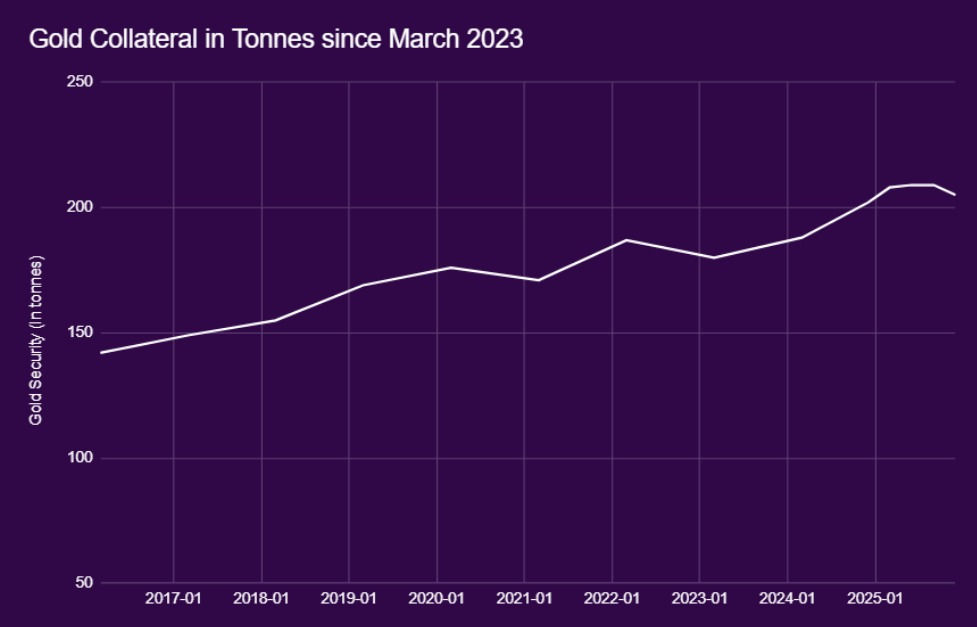

A more direct way to look at growth is to focus on the physical base of the business.

Gold held as collateral, the actual metal against which loans are issued, increased from about 180 tonnes in 2023 to roughly 205 tonnes in 2025. That is about 14% growth over the past two to three years.

Over the same period, the gold loan AUM grew by roughly 126%.

Placed side by side:

Collateral growth: ~14%

Loan book growth: ~126%

The gap between the two is largely explained by the price of gold, which also rose about four times over the same period.

This can resemble steady compounding, but it is closer to repricing than actual growth.

The persistence of high lending rates adds context. If expansion is being driven mainly by rising collateral values rather than improvements in efficiency or risk, the lack of downward pressure on pricing suggests the underlying economics are not as strong as they appear.

What Happens When the Cycle Reverses

If gold prices fall, collateral values fall with them.

For most of the past decade, loan yields stayed above 20% — notably high for a product backed by gold, one of the most liquid assets in the world. Rates only moved below 20% between FY22-23 and FY24-25, coinciding with what looked like genuine margin improvement.

The operational workload is driven by how many loans are being serviced, not what the collateral happens to be worth. As gold prices rose, the same loans against the same physical gold generated more revenue. Costs gradually fell but not because the operations got leaner rather, the same gram of gold pledged was unlocking a larger loan, reducing the workload per rupee disbursed.

A fall in gold prices would compress collateral values, forcing borrowers to top up their pledged gold or partially repay. Many wouldn't be able to, and the pressure would build quickly:

Defaults rise, asset quality deteriorates

Recovery efforts intensify, costs increase

Branch operating costs continue regardless of volumes

Revenues fall with the loan book. The cost base doesn't follow.

Even in a Benign Scenario

Assume gold prices do not decline.

If prices remain flat, the mechanism that drove prior expansion no longer contributes to growth. The outcome is not stability but a slowdown in underlying expansion.

If prices continue to rise, the business continues to benefit from the same external driver. In that case, performance remains dependent on a variable outside the control of the lender.

The business may not be compounding, but rather merely repricing.

What This Means

This is not a negative view on gold loan companies as a category. Many have durable strengths in distribution, customer relationships, and execution.

However, understanding the source of reported growth is necessary to assess its durability.

When a significant portion of performance is linked to a single external variable, in this case, gold price climbing:

Upside becomes dependent on that variable continuing.

Downsides emerge when those variable reverses.

Lower amount of loans

Higher credit costs

Lower interest income

Tighter funding conditions

Closing Thought

In markets, narratives tend to follow numbers. Strong loan book growth becomes a strong business narrative, and over time that narrative can take on a life of its own, increasingly detached from the underlying mechanics that produced it.

Good investing works the other way. It questions what lies beneath the numbers before the narrative has fully formed.

This is the first piece in our Risk Series, where we examine simple, often overlooked risks embedded in industries and businesses across the market.

Every portfolio has positions. Only a few have perspective.

Disclaimer: This article is for educational and informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any security.

Comments